Mortgage Rates vs. Housing Prices

Just how correlated are they? What you need to know.

Written by James V. Smith of Hughes Browne Group

You’ve probably heard from someone before (maybe even me), “real estate is hyper-local” - this is irrefutably true. However there are large macro trends that impact all real estate markets in the country. Different markets handle these outside pressures differently, which is why it’s important to not only understand individual regions and communities but also larger factors that drive home valuations.

A commonly cited factor impacting housing prices is mortgage rates - and for good reason. The two are inextricably tied. Mortgage rates, though, are only one of many factors impacting the value of housing over time, and those who predict that higher mortgage rates on their own will drive housing prices lower are usually wrong.

Some other notable factors:

- Unemployment

- Housing supply

- Lending guidelines

- Population changes (increasing? decreasing? changing demographics?)

- Rate of new construction

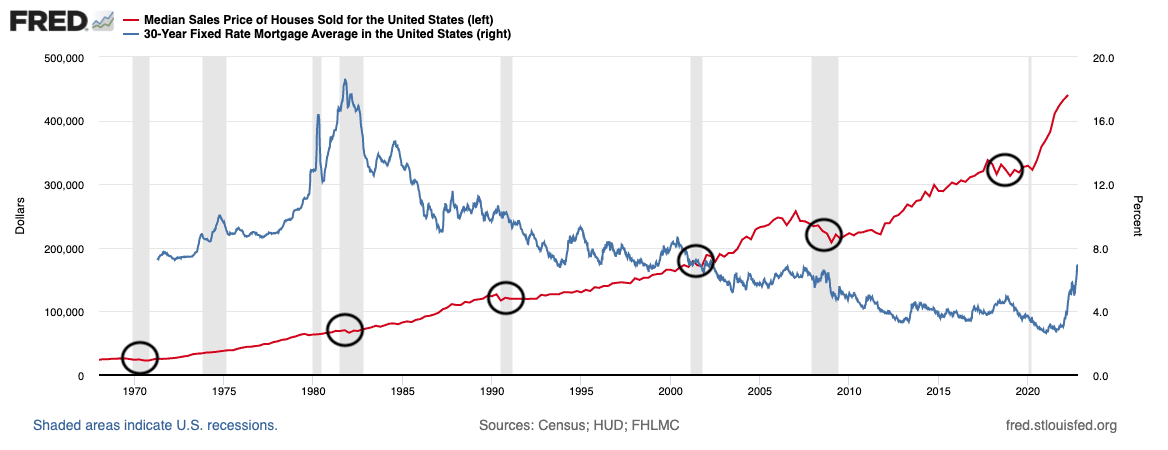

So, just how correlated are housing values to mortgage rates? Less than you might think. Take a look at the chart below, which shows the median sales price of a home sold in the United States vs. the 30-year fixed mortgage average. Since 1970, markets that saw a decrease in the median sales price of a home sold were more likely to have FALLING interest rates than rising ones.

The only real comparison for the scale of rate hikes we have seen recently are the Fed’s actions in the late 1970’s and early 1980’s to quash inflation. Because of the Fed’s actions and other factors including inflation, mortgage rates rose from 8.65% in 1977 to 18.63% in 1981. Over those four years of incredibly high rates, the median sales price of a home in the United States rose from $46,300 to $70,400 - that’s just over 52% growth!

This doesn’t mean our current market is primed for huge home price growth - but it does demonstrate the complex relationship between home values and mortgage rates.

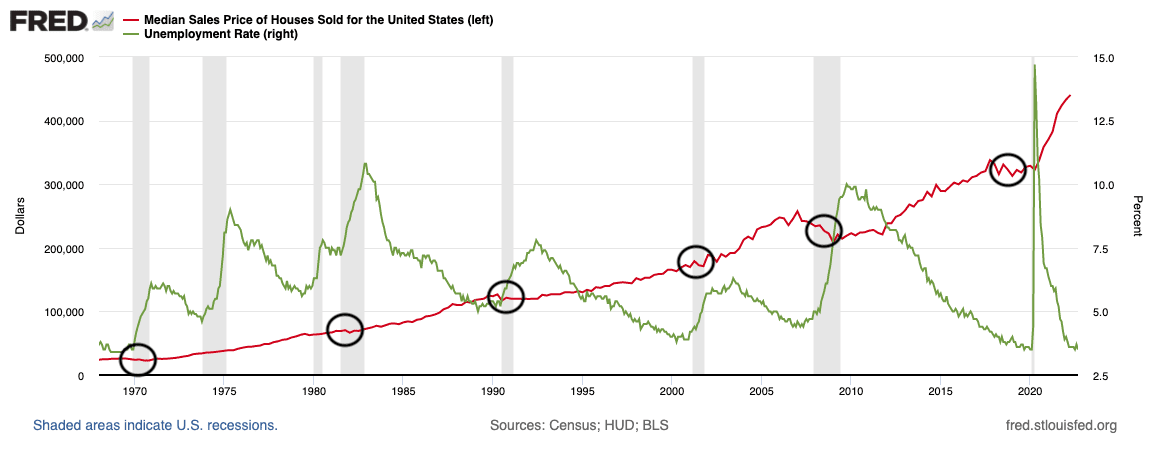

What other factors might impact the current housing market even more than mortgage rates? The chart below shows the same 6 highlighted markets as discussed above. Notice the strong correlation between unemployment and housing values. Since 1970 nearly every market that’s seen falling housing prices has also seen quickly rising unemployment.

To take it one step further, the United States has experienced 12 recessions since World War II. Each and every recession has shared two characteristics - a contraction of economic output, and a rise in unemployment. In regard to housing values, though, some recessions have seen falling home values, some have seen flat, and some have seen upticks. Check out these links to a great WSJ ARTICLE and WSJ VIDEO discussing the unique employment situation in today’s economy. How today’s labor market ultimately settles out will go a long way toward determining our odds of recession, as well as the possibility of declining housing prices.

Still, it’s obvious that rapidly rising interest rates will suppress demand for mortgages and therefore houses. More than half of homes purchased in the US are purchased with some type of mortgage. As the cost of financing rises, less consumers look to finance homes.

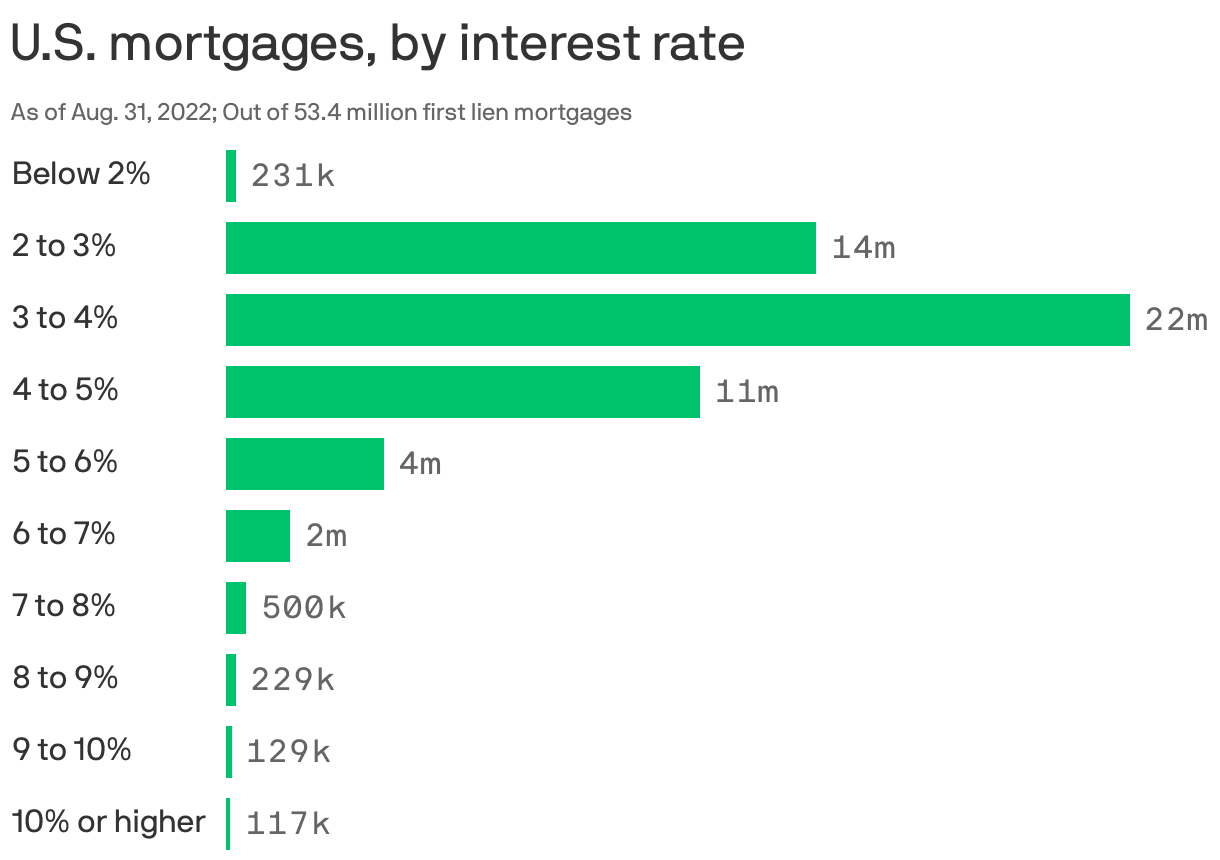

How, then, could home price values stay level, or even rise, in times of rising interest rates? To answer, we have to look at the supply side of the market. Higher mortgage rates disincentivize homeowners who might otherwise become sellers. As of July 31, nearly nine of every 10 first-lien mortgages in the US had an interest rate below 5% and more than two-thirds had a rate below 4%. About 83% of those mortgages are 30-year fixed rates. (from mortgage-data firm Black Knight Inc.).

Chart: AXIOS Visuals

Homeowners currently holding a mortgage at 3% (or below) are far less likely to sell and take on a new mortgage at a significantly higher rate. This constricts the supply of homes for sale, therefore buoying prices. WSJ recently described the situation as an example of “Golden Handcuffs”.

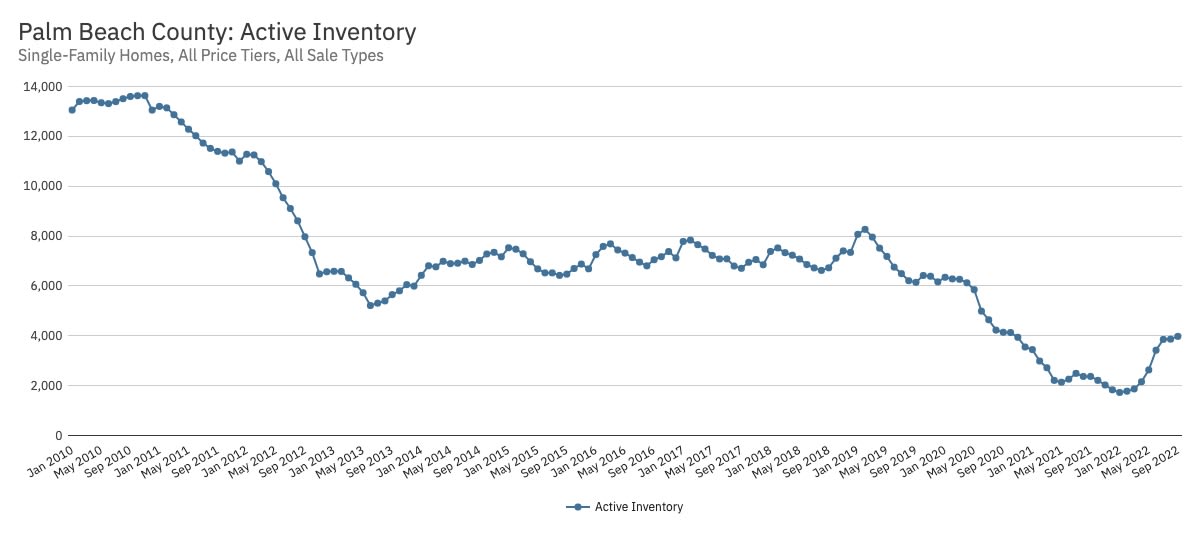

The current Palm Beach County market shows the impact of these “golden handcuffs” on inventory. While inventory has come up from the historic lows of last year, the growth of inventory has plateaued, as evident on the chart below. In the 8 years prior to the pandemic it was typical to have around 7,000 active listings of single family homes in Palm Beach County. Over the last few months it appears the market is settling in at around 4,000 active listings.

The limited inventory in Palm Beach County, coupled with high demand from retiring baby boomers, millennials reaching prime home-buying age, snowbirds avoiding the cold, and the continued migration and corporate relocation from high-tax states, means the odds of a large housing slump are low.

While real estate will always be hyper-local, the overarching trends impact all markets. It’s crucial to understand how these large market forces impact different regions and communities in order to make confident decisions regarding real estate purchases and sales. If you're considering buying or selling, or would just like to discuss how these large trends might impact your market, please reach out!

*Disclaimer* - Compass is a licensed real estate broker. All material is intended for informational purposes only and is compiled from sources deemed reliable but is subject to errors, omissions, changes in price, condition, sale, or withdrawal without notice. No statement is made as to the accuracy of any description or measurements (including square footage). This is not intended to solicit property already listed. No financial or legal advice provided. Equal Housing Opportunity.